What inflation could mean for annuities

« Return to News

It’s a scary time for many people to be thinking about retirement, and not only because of an ongoing pandemic that has radically changed our daily lives.

Along with that, inflation is a potential threat to retirees living on fixed incomes and workers nearing the end of their careers. Add in the possibility of stagflation sluggish economic growth coupled with inflation and things get more complicated.

Inflation can have a real impact, said Todd Giesing, assistant vice president and director of annuity research at the Secure Retirement Institute. When you think about the cost increases were seeing today, it absolutely is hitting the pocketbooks of Americans. You can see it at the grocery store. You can see it at the gas pump. It is everywhere.

Many clients are almost certainly wondering what it means to their ability to retire and what they should do if inflation persists.

A quarter of more than 1,100 people surveyed in November by Allianz Life cited rising inflation as the biggest risk to retirement, up from 8% who said the same last year.

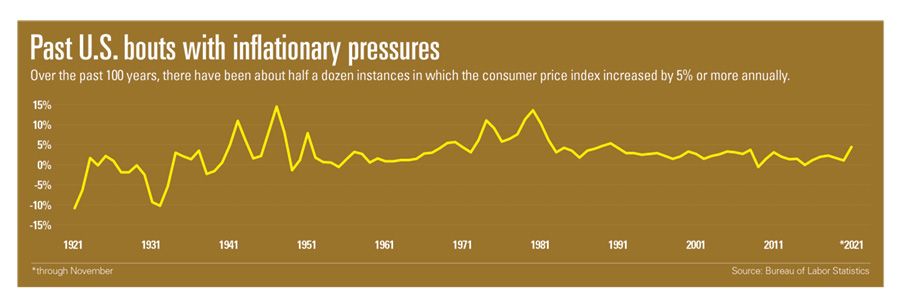

It’s still the early days of what could be a sustained period of price hikes, and its unlikely that many of the people facing the biggest risks have made major financial decisions in response to that trend, observers say.

And that means its prime time for advisers to start having conversations with clients about how inflation could affect their plans and what they can do to minimize their risks.

Among the questions is whether they should be considering annuities. For those who already have contracts, a concern could be whether they would be better off swapping out products.

For a future retiree, inflation can be a concerning issue, particularly because no one knows how long they need to fund their retirement income for in other words, when will you die? Steve Parrish, co-director at The American College Center for Retirement Income, wrote in an email.

Were sitting on a hot stock market, and if the [Federal Reserve] raises rates, this may cause the market to cool off,” Parrish wrote. “I know of a couple of savvy pre-retirees who are, largely because of inflation concerns, taking some of their equity gains and placing the proceeds in a deferred income annuity.

That could be done with nonqualified money through a brokerage account, for example, or with tax-qualified assets, through a qualified longevity annuity contract, he noted. Like other annuity purchases, that can help ensure someone keeps receiving cash payments.

You peel off gains now so that youll have money in the future money you may particularly need because some of your other income sources have either been exhausted, lost value or lost spending power, Parrish said.

INFLATIONARY EFFECT

Even normal inflation has an impact on finances in retirement. Spending decreases by an average of 12% over 20 years for a retiree, although that affects people with lower wealth much more substantially, a recently published working paper from the Center for Retirement Research at Boston College found. In short, the researchers found that retirees spend less over time out of necessity.

This is a prime time to talk to clients, especially those that are five to 10 years from retirement, about the ability to build protection, said Kelly LaVigne, vice president of advanced markets and solutions at Allianz Life. When inflation goes up, its very difficult for everyone, but for those on fixed income it’s more difficult.

Interest-rate-dependent products, which include fixed annuities, guaranteed benefits on variable annuities and others, can provide more attractive features in response to a move from the Fed, he said.

We know that if inflation goes up, the Fed is going to act. Theyre going to increase interest rates Thats good for the insurance companies as a whole, LaVigne said.

You might be able to move a traditional fixed client into a fixed indexed product, simply because it will give them a little bit more opportunity to at least mitigate the risks associated with inflation.

Products that provide increasing payments over time can help, although those features usually offer lower initial payment rates than fixed annuities do, he noted.

While many people hold annuity contracts that were purchased when the guaranteed benefits available with some products were in their prime, it is unlikely that VAs will see the richness of their optional riders rise to pre-financial-crisis levels. Prior to 2009, insurers offered VAs with very competitive features that many providers later regretted, when interest rates fell.

The days of those income wars or benefit wars are pretty much over, LaVigne said. As an industry, we really have learned our lessons from the past.

RISE OF RILAs

Insurers are now more interested in buffered annuities registered index-linked annuities (RILAs), as they have been rebranded, a type of VA that limits an accounts growth potential but also has guardrails on losses. Those products account for a small fraction of all annuity sales, but demand has increased quickly over the past few years, with market volatility and overall uncertainty serving as selling points. Annuity providers have been adding RILAs to their product rosters in droves.

For the first nine months of 2021, RILA sales were 81% higher than the same period in 2020, data from Limras Secure Retirement Institute show.

Of course, annuities are only one area for advisers to make recommendations to help risks associated with inflation, Giesing said.

Heightened inflation is still something fairly new, so I dont see people rushing to change strategies immediately, he said.

And so far, there are no indications that the current heightened inflation has prompted any increased demand for annuities, Sheryl Moore, CEO of Moore Market Intelligence, said in an email.

We are just showing normal, cyclical growth at this point, Moore said.

Compared with what products were on the market during high inflation in the 70s and 80s, there are many more options today, Giesing noted.

We didnt have the suite of products that are available today, on the annuity side or other products, to try to find that balance between protection and growth, he said.

Inflation will drive asset allocation

The post What inflation could mean for annuities appeared first on InvestmentNews.

Have any Questions?

We're here to help. Send us an email or call us at +1 (585) 329-9661. Please feel free to contact our experts.

A donation will be made by Adviser First Partners to a Veterans organization on behalf of all financial professionals and firms that register each month

Contact UsSubscribe to our mailing list.

![]()

© 2024 Adviser First Partners. All Rights Reserved.

Web Design by eLink Design, Inc., a Kentucky Web Design company