Big buildup of savings could rein in rates

« Return to News

The economic shock from the coronavirus caused companies, consumers and investors to hoard cash like almost never before.

Many experts expect that urge to save to stick around for the long haul. And that should create strong demand for the safest fixed-income products, a force that could lend a hand to the Federal Reserve when it comes to suppressing yields as the government ramps up its supply of bonds to pay for economic stimulus measures.

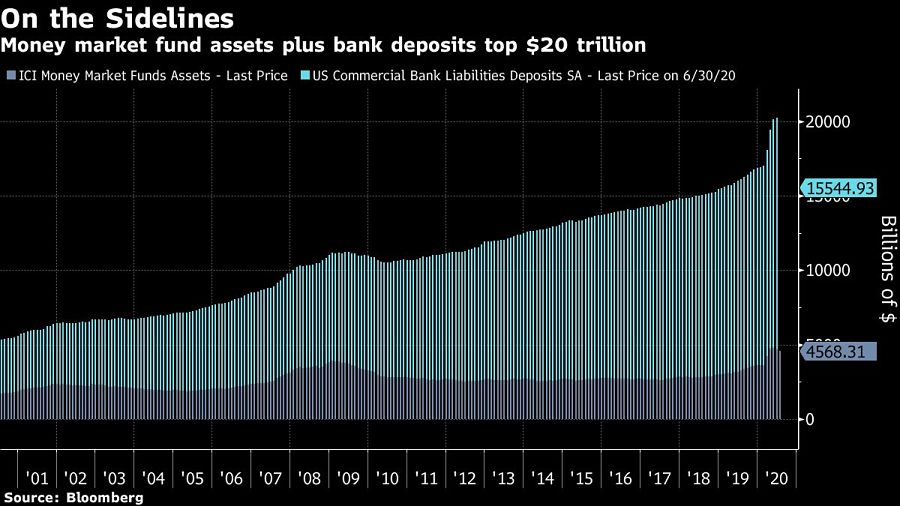

Deposits at U.S. commercial banks have surged by 18% this year to a record $15.6 trillion, according to Fed data. The flood of cash into money-market mutual funds has subsided, but at $4.6 trillion the total is still nearly $1 trillion larger than before the pandemic, Investment Company Institute data show.

Anthony Crescenzi, a portfolio manager at Pacific Investment Management Co., is among those saying that uncertainty about the economy will keep cash accounts bloated.

“The high savings rate exists in part due to the caution that households are taking with respect to expenditures, a factor that is likely to persist for some time,” said Crescenzi. “The presence of a substantial amount of savings deposits on bank balance sheets is likely to impart downward pressure on market interest rates.”

The effect won’t just be limited to money-market rates, according to Crescenzi. Since banks also hold significant investments in longer-dated assets such as Treasury notes and bonds and agency mortgage-backed securities, the deposit glut should create demand — and hence low yields — for those assets as well.

Commercial banks occupy an increasingly crucial niche for fixed-income purchases. The global surge in sovereign debt to finance stimulus programs is testing even the voracious appetite of the world’s central bankers, with about $1 trillion coming to market in the months ahead that still lacks buyers.

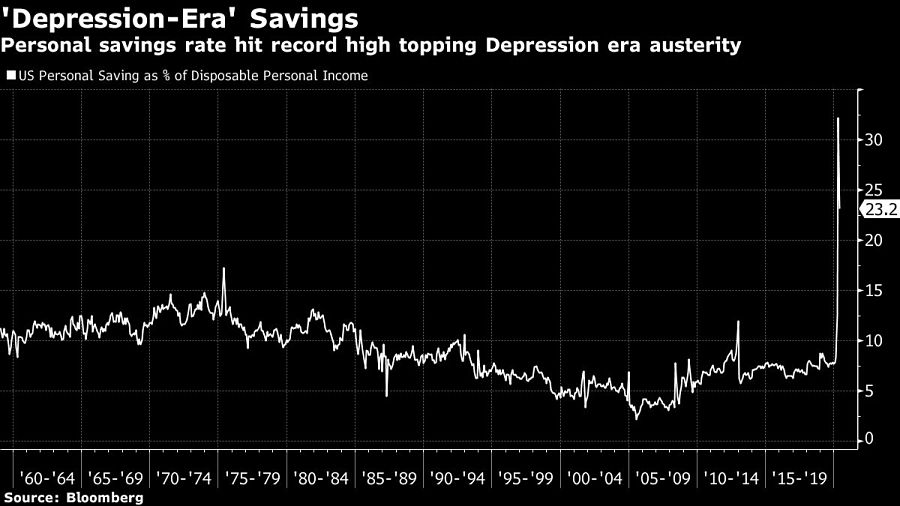

One key variable will be the personal savings rate in the U.S., which shot up to 32.2% in April — the highest in Commerce Department records dating back to 1959 — as the economic shutdown reduced or eliminated many outlets for spending. The rate slipped back to 23.2% in May, but many analysts and investors expect it to stay elevated above last year’s average of about 8%.

Danielle DiMartino Booth, author of “Fed Up: An Insider’s Take on Why the Federal Reserve Is Bad for America” and founder of the Quill Intelligence research firm, likens this year to the Great Depression, a slump that was followed by an era of austerity and increased savings. While that may provide a financial cushion and a sense of security for savers, it very well could be a headwind to the rebound in the world’s largest consumer economy as a higher baseline savings rate is created.

“A lot of people are going to reexamine how they view money,” Booth said. “You are going to have a marked shift upward permanently in the propensity and the desire to save, which is not something we are used to in an economy that is normally about 70% consumption.”

The long-lasting psychological scars of this crisis mean that the savings rate should likely stabilize at about 15%, or double its historic average, said Peter Yi, director of short-duration fixed income and head of credit research at Northern Trust Asset Management.

‘REALLY AFRAID’

He watched the assets in his own firm’s money-market mutual funds surge by 50% last quarter to $183 billion. The reluctance to spend applies to corporations as well as individuals.

“Companies are really afraid of what this downturn can mean and are drawing down their bank credit lines and trying to strengthen their liquidity profile during this extremely uncertain operating environment,” Yi said. “People overall are still concerned, with some investors simply saying they need to get on the sidelines until the dust settles.”

Risk aversion and economic uncertainty are not the only reason to believe balances in the safe harbors of money-market funds and bank deposit accounts will remain swollen, according to Goldman Sachs. The Treasury yield curve is much flatter than it was in the aftermath of previous recessions, which reduces the opportunity cost of holding short-term bonds compared with long-term securities, Goldman analyst Alessio Rizzi and colleagues wrote in a July 17 note.

Although only a handful of the highest-yielding money-market funds and bank savings accounts are paying more than 1%, according to Bankrate.com, Treasuries with a maturity of less than 20 years are yielding below that.

PRICEY STOCKS

Lofty valuations on equities also raise doubts about the ability of the stock market to lure more cash from the sidelines. The S&P 500 is trading at its highest price-to-earnings valuation in a decade, while the Nasdaq 100 Index hasn’t been this expensive compared with reported profits since January 2005.

And compared with long-term history, the allocation to equities relative to total money supply is elevated and that means the potential for returns remains low, the Goldman analyst wrote.

“There’s a dynamic where, while the stock market may have recovered a great deal of the downward performance from March, there’s still a sense out there that the risks are generally unknown,” said Brett Wander, chief investment officer for fixed income at Charles Schwab Investment Management, which manages $3.85 trillion.

The fiscal piece of the equation is key since many investors assume further stimulus is on its way, but concerns are emerging about a reckoning to come should the financial cushions established in the second quarter disappear or be reduced. And another round of fiscal stimulus may just kick the can down the road if savers are unwilling — or unable — to go out and spend.

It all adds up to a “savings shock” that means it won’t just be the Fed’s monetary accommodation that continues to suppress interest rates, said Michael Darda, market strategist at MKM Partners.

[More: Here’s how target-date funds have fared as the market fell, and rose, in 2020]

The post Big buildup of savings could rein in rates appeared first on InvestmentNews.

Have any Questions?

We're here to help. Send us an email or call us at +1 (585) 329-9661. Please feel free to contact our experts.

A donation will be made by Adviser First Partners to a Veterans organization on behalf of all financial professionals and firms that register each month

Contact UsSubscribe to our mailing list.

![]()

© 2024 Adviser First Partners. All Rights Reserved.

Web Design by eLink Design, Inc., a Kentucky Web Design company